.jpg)

A Forgivable Promissory Note (FPN) is a different form of seller financing. Basically, it's a loan extended by the seller, which can be forgiven based on post-close metrics of the business.

.jpg)

A couple weeks ago, I wrote about how critical seller's notes are to your SMB acquisition, and why you probably shouldn't work with a seller who won't at least consider making a small portion of the acquisition price a seller's notes. Read that full piece about whether the business owner won’t consider a seller’s note.

This week, I'm taking it a step further with the Forgivable Promissory Note.

The FPN is a form of seller financing that the buyer won't have to pay back if the business doesn't hit predetermined metrics.

It allows buyers to offer a higher price for a business, but with less downside risk. Meanwhile, sellers benefit from increased purchase prices and potential tax advantages. The main tax advantage would be that proceeds are split over several different years, instead of the year of the close, meaning the seller's effective tax rate would be lower.

Both parties benefit, in theory, thanks to the greater alignment of incentives. With an FPN in the mix, the seller has a greater incentive to complete their post-close consulting to ensure the transition of ownership goes smoothly.

Eli Albrecht explained FPNs extremely well in this post about The Forgivable Promissory Note (FPN), which I encourage you to read. Here are a few of the important points that Eli highlights:

- FPNs are typically 10 to 20% of the purchase price

- Interest rates are usually 5 to 10%

- Buyer brings less cash to closing, but seller can actually walk away with more cash at closing (by removing an escrow)

What does forgiveness look like?

During negotiations, both parties would agree on a metric (or a combination of metrics) to base forgiveness on.

Some common ones include:

- EBITDA (best for buyer, but not seller)

- Revenue

- Gross Profit

- Customer Retention

- Employee Retention

- Seller performance on post-close consulting (if applicable)

Do SBA 7(a) loans allow FPNs?

Yes, but all metrics must be based on historical financials.

Example

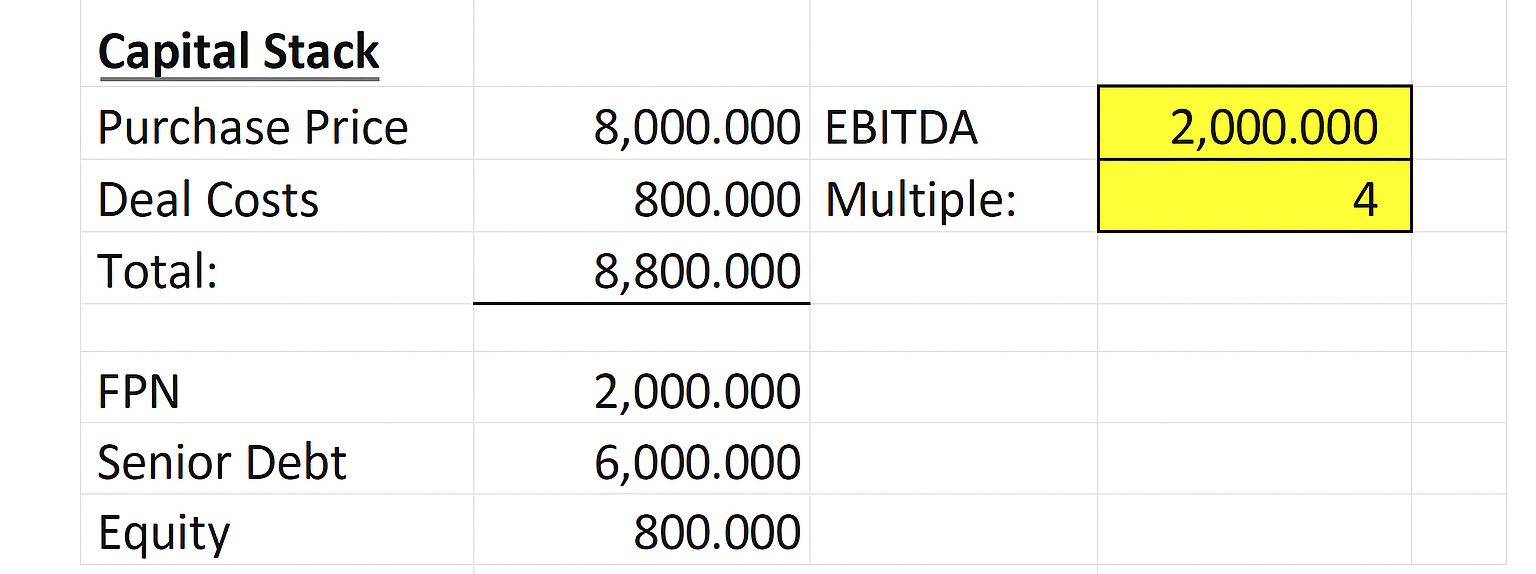

A non-financial sponsor acquired a company through a stock purchase with an F-Reorg. The purchase price was structured with: Promissory notes, SBA 7(a) loan, and equity from investors.

The transaction was successfully closed thanks to the excellent relationship between the buyer and sellers, a 'sign and then close' approach, and, most importantly, the expertise of the bank's attorney. The buyer ultimately owned over 80% of the business with a personal investment of $50,000 at closing.

The excellent relationship plays an important role here: You can't always have one of those between buyer and seller, but an FPN can help align the incentives of the two parties and make the post-close process easier for both, while helping to make sure the buyer is successful post-close.

Subscribe for

New Blog Posts

New Blog Posts

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.